Britain's economics consultancy trade, anchored by a £2.48bn disclosed-revenue floor and reconstructed from 8,293 filing events at Companies House in Cardiff.

90

Firms

£2.48bn

Revenue floor

8,293

Filings

25 yrs

Of history

↓ SCROLL TO BEGIN

Walk past 199 Bishopsgate on a weekday morning and you pass a glass tower whose tenants include RBB Economics. No sign on the door explains the economics underneath it. RBB Economics' FY2025 accounts show 18 LLP members, average profit per member above £3m, and a highest-paid-member disclosure of £5.77m.

That is the kind of number this series is built around: large enough to matter, public enough to verify, and hidden inside accounts that few readers outside the sector would naturally open.

RBB Economics is one example of a trade that remains obscure outside specialist legal, regulatory and policy work. 90 outfits sit in the curated catalogue of UK economics consultancies; the public directory gives 81 a direct Companies House number, while the working database also carries registered, parent and brand rows for analytical continuity. Across the latest disclosed-turnover rows in that database, 30 firms sum to £2.48 billion, an observed floor because many of the remaining firms file accounts without publishing a clean turnover line. Cebr's March 2018 estimate of £1.53 billion for 2016/17, extrapolated forward at the 11.3% CAGR they assumed, would imply roughly £3.6bn by 2025; the two numbers bracket a credible £2.5bn–£3.6bn band for the 2025 market. These firms advise competition authorities, law firms, regulators and governments, often in merger reviews, regulatory proceedings and litigation. The work is visible in public filings and case records, but rarely as a familiar consumer brand.

The paper trail, however, is another matter. UK-registered firms file accounts at Companies House in Cardiff, where they become public, indexed and free. The last twenty-five years of those filings run to 8,293 filing events, including 1,664 account filings; the extracted financial series contains 1,335 account-year rows. Thirteen charts carry the story.

CHAPTER 01

The shape of the market

A 90-firm public catalogue, grouped by what each firm does and sized where current turnover is visible.

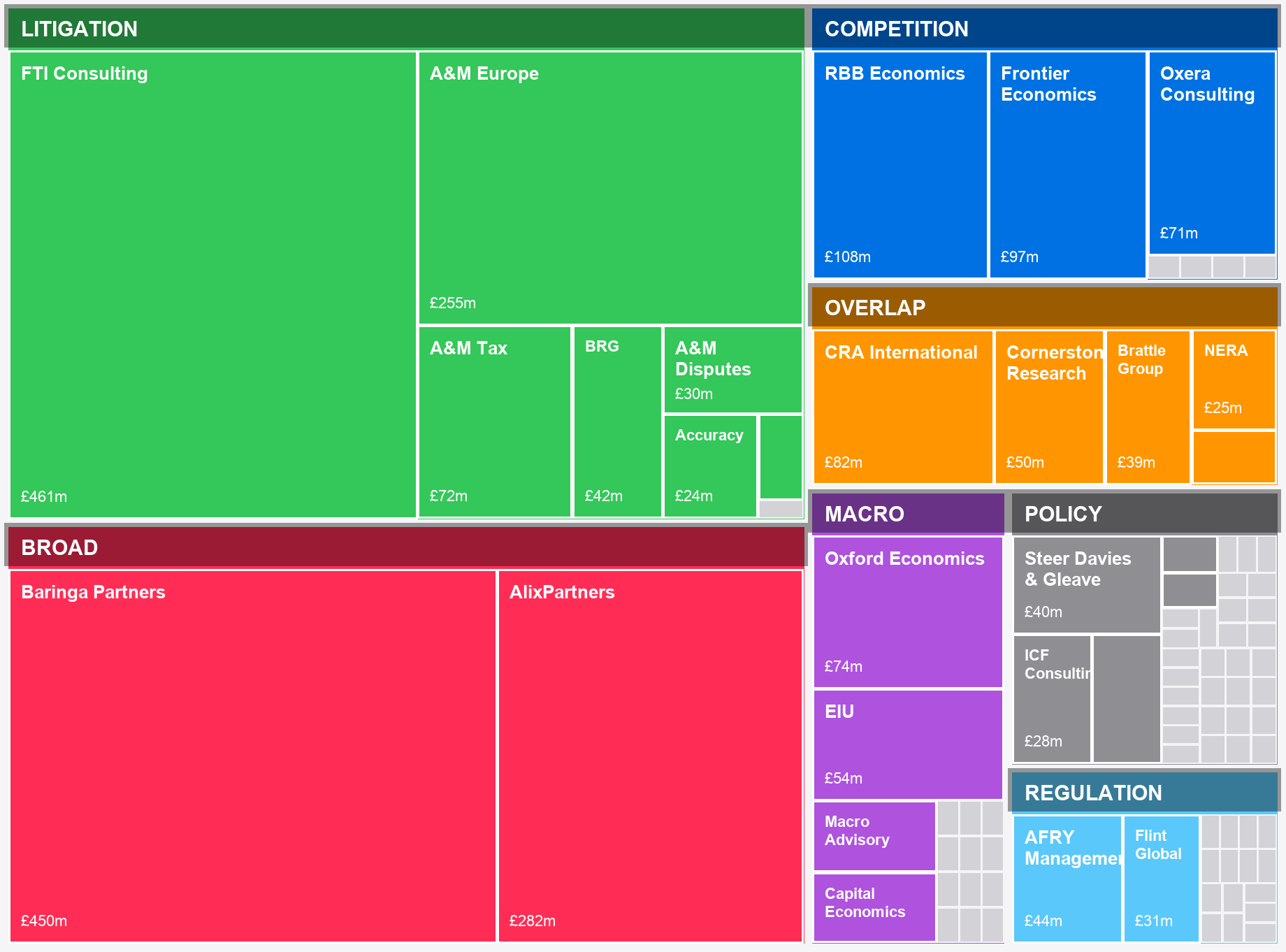

UK Economics Consultancy Universe

N=90 · GROUPED BY SEGMENT · SIZED BY LATEST UK REVENUE

TREEMAP

View on a laptop for the interactive chart.

The public catalogue is grouped into seven segments. Policy has 35 firms; regulation has 17; and macro forecasting has 16. Litigation and competition together account for 15 firms, including several high-revenue rows.

Block size is turnover, where turnover is visible. In this chart, the largest measured rectangles are the multi-practice advisory houses: FTI Consulting, Baringa and A&M. The pure-play economics shops, the boutiques that trade on formulas, expert reports and witness evidence, sit as medium blocks inside their own colour band.

THE INVISIBLE TAIL

The firms outside the disclosed-turnover set are carried as unsized rows where this project has no clean current turnover line. They appear in the treemap as identical uniform tiles, ranked by category rather than revenue.

The visible market is the measurable part. The rest of the catalogue still matters, but the accounts do not let it be sized cleanly.

CHAPTER 02

The league table

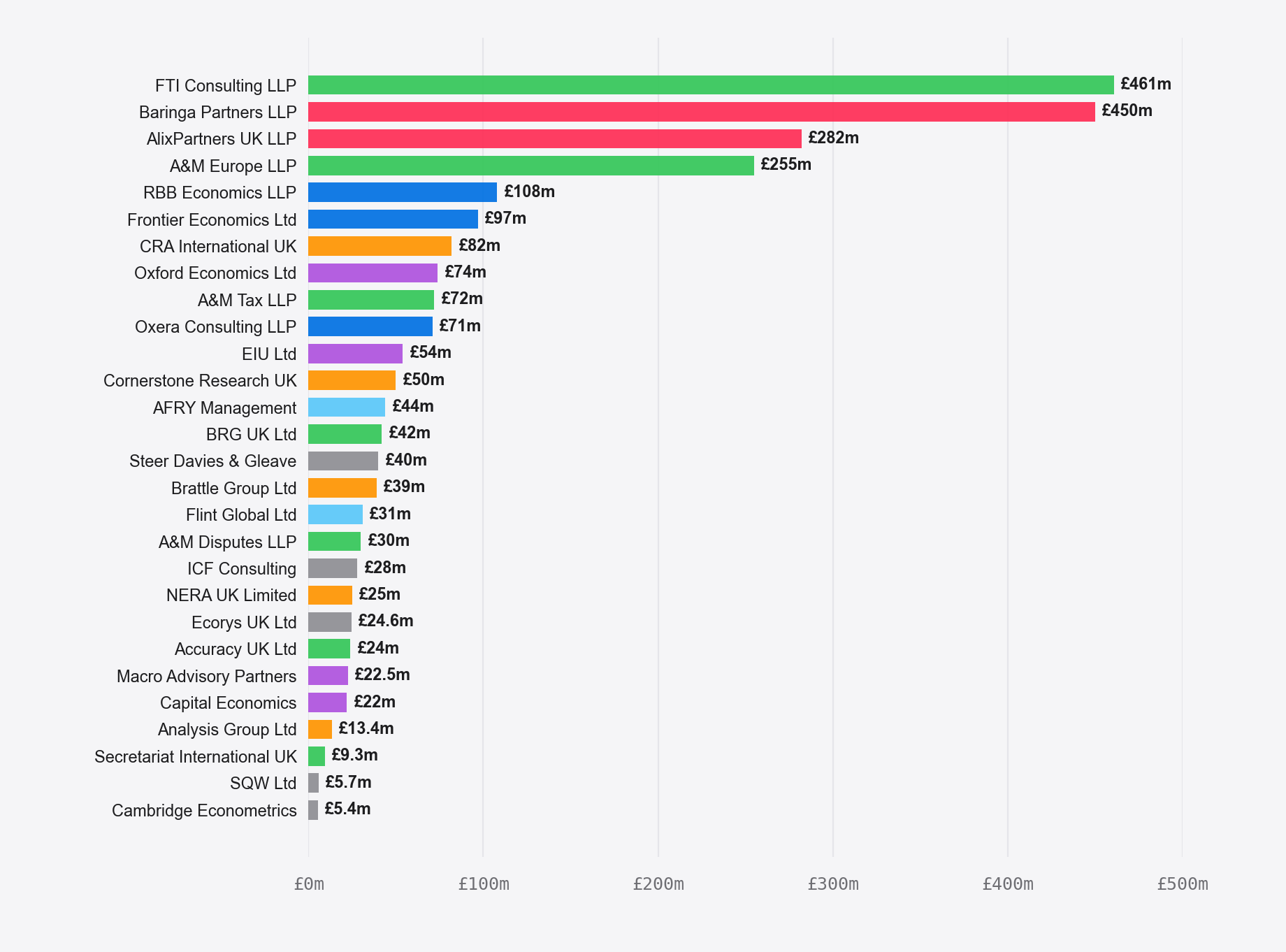

Across the CH-tracked database, 30 firms carry a positive latest turnover disclosure; 28 of those exceed £5m on the canonical series once estimate-only rows are set aside. The 28 ranked here are the cleanest single-year readouts. The remainder are excluded from this chart because the project ledger marks them as no clean current turnover line, estimate-only, parent or consolidated accounts, or small-company, charity or academic forms that do not expose practice revenue — the long tail covered in Part 5.

Revenue League Table

£ MILLIONS · LATEST FILED YEAR · SOURCE: COMPANIES HOUSE

BAR CHART

View on a laptop for the interactive chart.

Above £250m sit four giants. In the filed-account chart, FTI Consulting LLP is the largest measured row at £461m (Companies House OC372614, for the 12 months to March 2025; the prior-year comparative of £550m covers a 15-month transition period from 1 January 2023 to 31 March 2024 and is not directly comparable on a YoY basis); Baringa Partners is second at £450m; AlixPartners UK follows at £273m (net revenue, after client expenses and disbursements); A&M Europe rounds the quartet at €301m (~£255m). These are multi-practice advisory firms rather than pure economics boutiques. Each runs economics beside restructuring, forensic accounting or management consulting, and it is the bundle that generates the scale.

The pure-play tier begins with RBB Economics at £108m, followed by Frontier at £97m, CRA at £82m, Oxford Economics at £74m and Oxera at £71m.

Between roughly £22m and £44m there runs a middle tier of US-parented firms, European subsidiaries, transport and policy specialists, and macro shops: AFRY, BRG, Steer, Brattle, Flint Global, A&M Disputes, ICF, NERA, Cornerstone, Ecorys, Accuracy, Macro Advisory and Capital Economics. Cornerstone Research files in US dollars, so its £28m figure is currency-converted (FY2024 turnover $35.4m at ~£0.79/$). Below that, the disclosed list thins to Analysis Group, Secretariat, SQW, Cambridge Econometrics and a handful of smaller or older rows; everyone else sits outside the clean-turnover ranking because the public filings do not expose a comparable revenue line.

CHAPTER 03

The margin spectrum

From loss-making to highly profitable. The same industry contains both extremes.

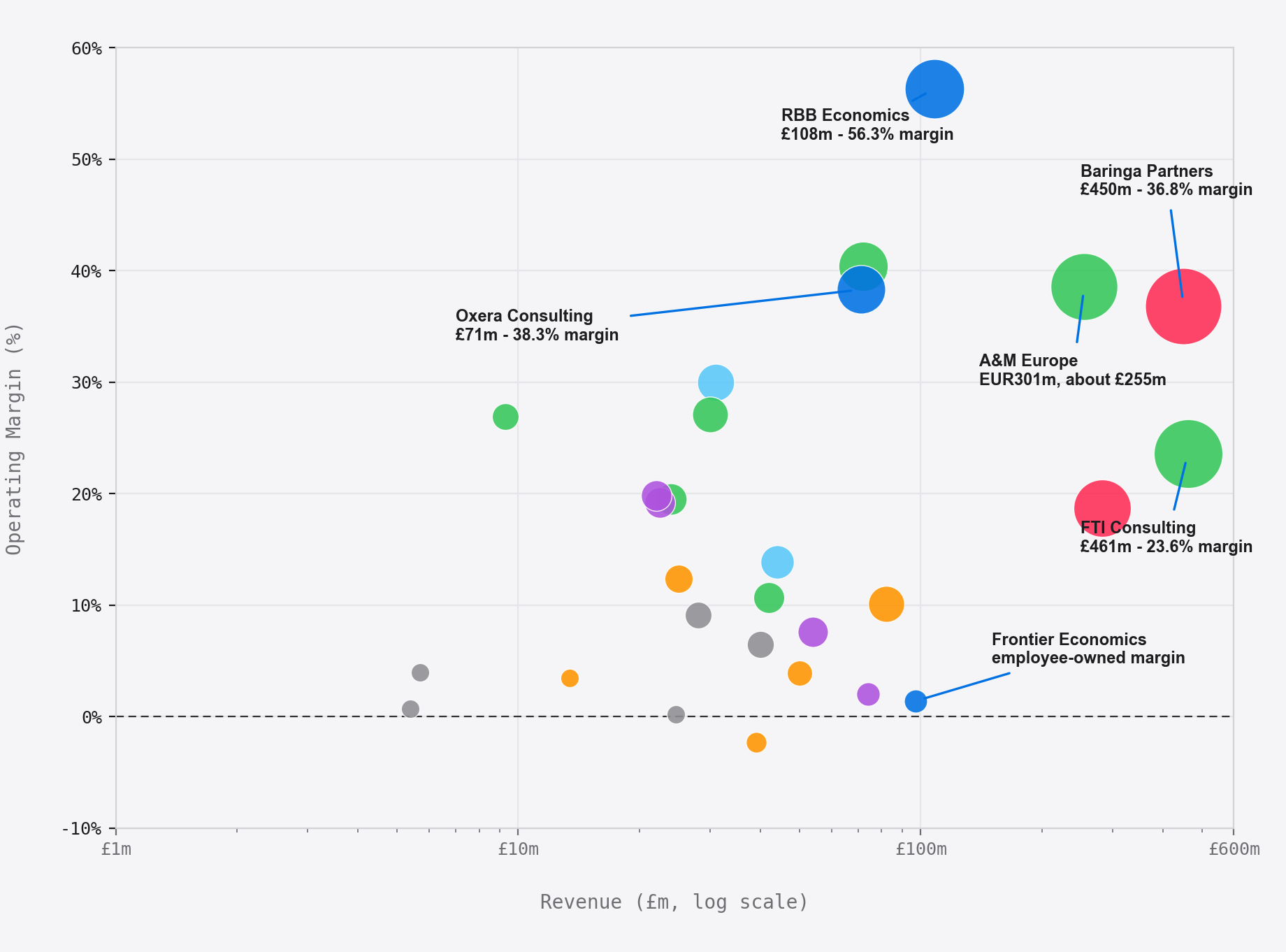

Operating Margin vs Revenue

SCATTER · BUBBLE SIZE = OPERATING PROFIT

SCATTER PLOT

View on a laptop for the interactive chart.

RBB sits by itself in the top right corner. A 56 per cent operating margin on £108m of turnover is a combination nobody else in the dataset gets near. The firms that match RBB on margin are a fraction of its size; the firms that match it on revenue carry margins that are half as wide.

A cluster of mid-sized names, Oxera, Baringa, A&M Europe, A&M Tax, Flint Global, runs along the 30 to 40 per cent band. These are the places where partner economics actually work: enough revenue to matter, enough margin to reward.

Frontier Economics and Oxford Economics anchor the bottom. Frontier at £97m, 1.4 per cent margin. Oxford Economics at £74m, 2 per cent margin. The numbers look alarming until you read the ownership footnote.

Frontier is not under-earning. It is employee-owned, and it distributes its operating surplus through salaries rather than profit; the margin line is a residual by design. Brattle UK is the loss-making row in this chart, with a £0.9m operating loss on £39m of revenue. The remaining plotted firms reported positive operating profit.

A caveat on comparability. The margins plotted here are as reported in each firm’s filed accounts. In the project’s accounting notes for the LLPs in the set (RBB, Oxera, Baringa, FTI, A&M, AlixPartners UK), operating profit is treated as the pre-members’-remuneration line, so the RBB 56.3% and Oxera 38.3% values are computed on the same operating-profit basis. What differs is how each firm classifies what flows below operating profit: RBB £0, Baringa £0, Oxera £8.3m as members’ remuneration. On a distributable-profit-over-turnover basis the comparison bifurcates: RBB 55.6%, Baringa 36.0% (each essentially equal to its operating margin, with neither charging below-line rem), Oxera 26.5%. The RBB–Oxera gap widens on that basis from 18 to roughly 29 points. The Ltd companies (Frontier, Oxford Economics, Capital Economics, Brattle UK) report post-owner-remuneration margins, which is a different basis. Read the chart for where each firm routes value.

CHAPTER 03B

The long view

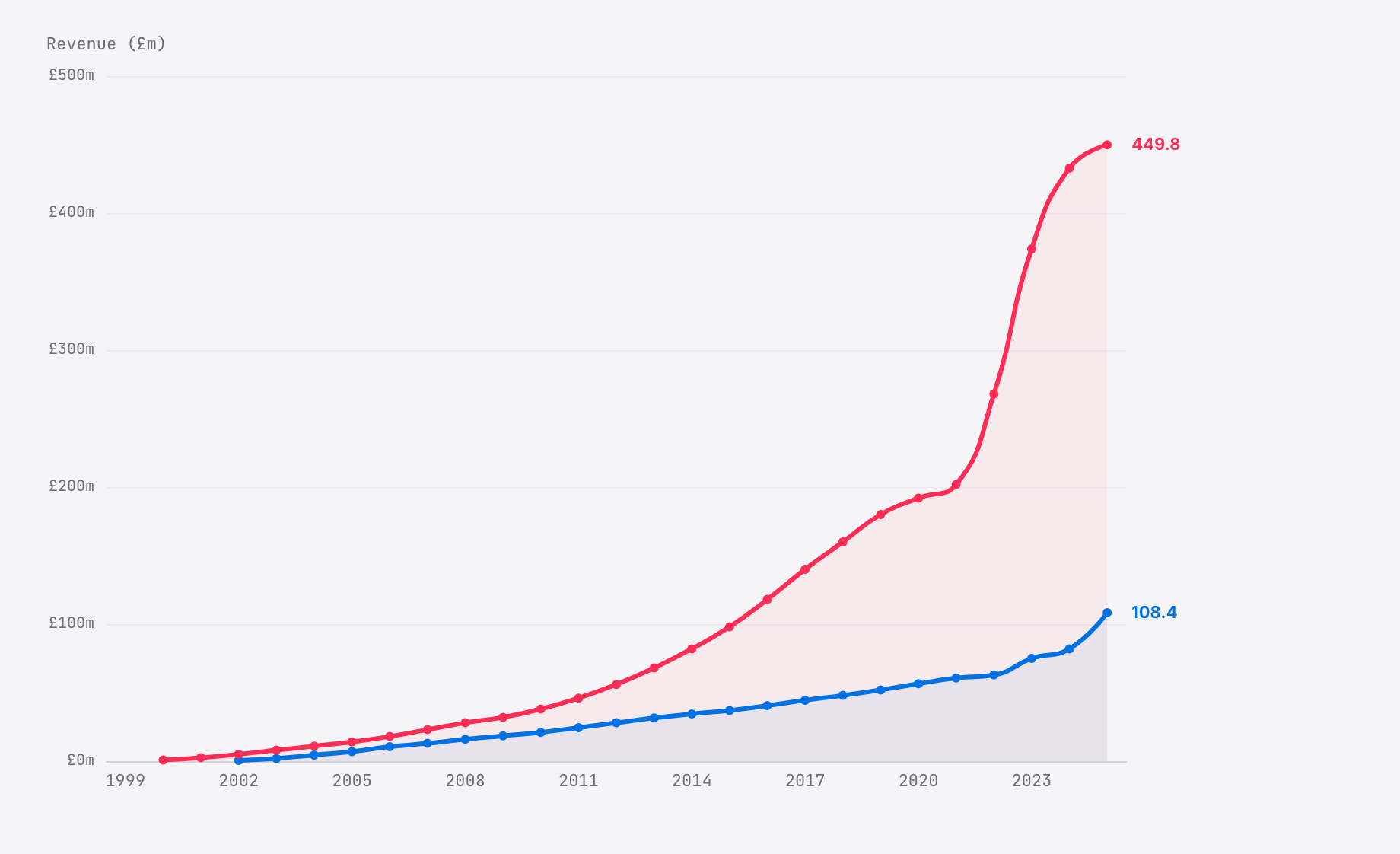

Revenue since each firm was born. Frontier 1999. Baringa 2000. CRA's UK entity 2000. RBB 2002.

Revenue since founding

£ MILLIONS · ANNUAL TURNOVER · 1999 → 2025

HISTORICAL LINE

View on a laptop for the interactive chart.

RBB's early line is an estimate, not a filed-account series.RBB says it was established in 2002 by Derek Ridyard, Simon Bishop and Simon Baker, starting with 16 people. The chart begins with an illustrative £2m point in 2003 and an illustrative £21m point in 2010; the hard filed-account section starts with FY2020, where the accounts show £59m, and runs to £108m by FY25.

Baringa started smaller and scaled faster. A management-consulting generalist from day one, it crossed £100m in the mid-2010s, £200m in 2021, and approaches £500m today. Its partner ranks roughly doubled alongside that growth: the average number of members rose from 98 in FY2021 to 180 by FY2024 (and 178 in FY2025), verified against the firm’s Companies House accounts. That near-doubling was organic scaling rather than any one-off — turnover (£202m to £433m) and staff (about 810 to 1,820) grew in lockstep, as a partner-owned LLP that promotes consultants into membership rode a post-COVID surge in energy-transition, financial-services and government work and built out US, Irish and Bulgarian hubs. It is a separate story from the firm’s FY2022 profit spike, which was a one-off £74.4m gain on selling a climate-modelling software business. In the filed-account series, the two firms therefore show two different working models rather than one common template.

The early-year figures for RBB, Baringa and Frontier are approximations reconciled against each firm's own published histories; their recent data points (RBB from FY2020, Baringa and Frontier from FY2021 onwards) are read from Companies House filings. The CRA (UK) line is different in kind: it is filed Companies House turnover throughout, from £7.5m in FY2002 to £82.4m in FY2024 (FY2025 not yet filed), and is one of the longest fully filed series in the project database.

CHAPTER 04

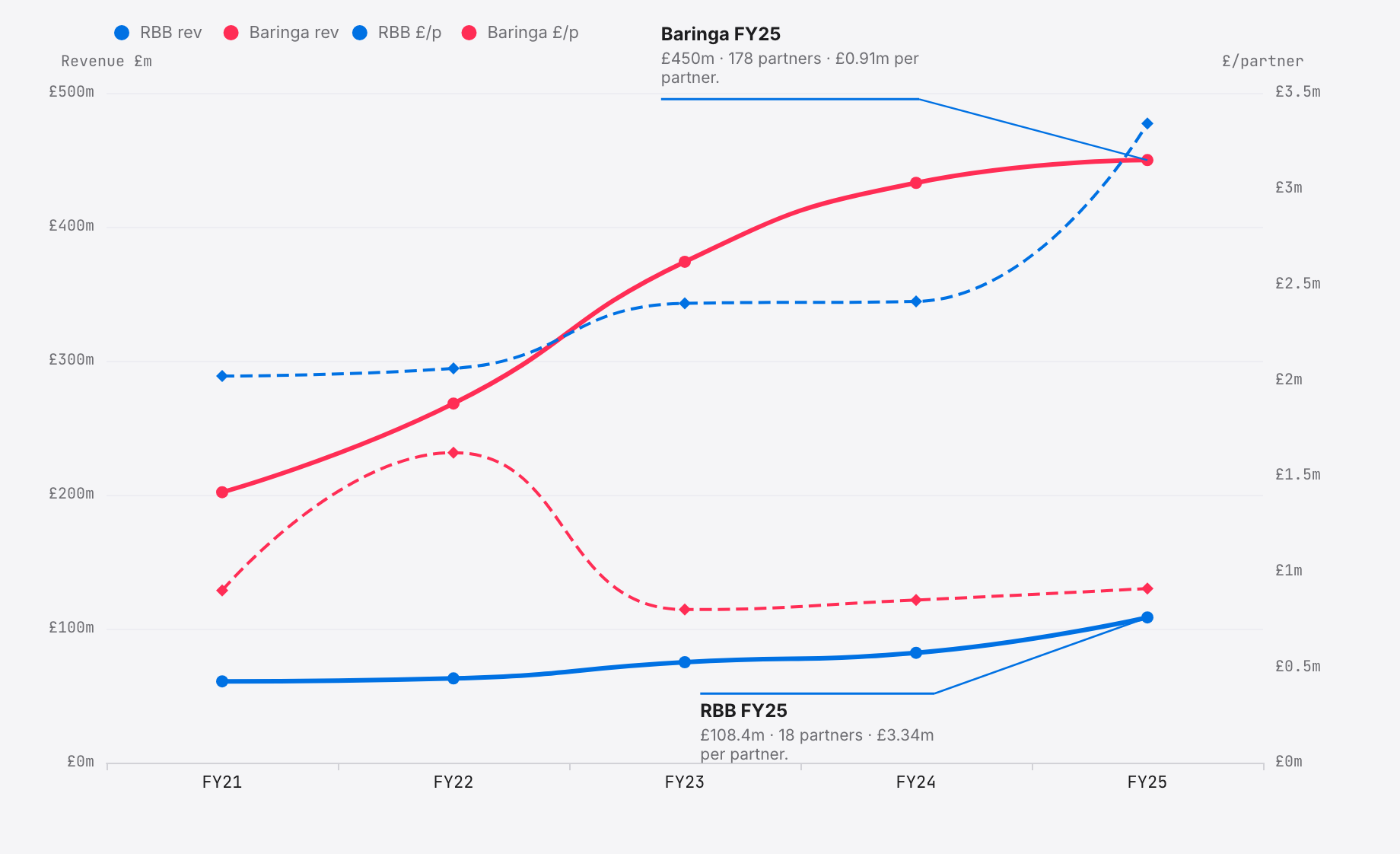

Two ways to grow

RBB and Baringa, side by side, 2021 to 2025. And then the arithmetic underneath.

Revenue Growth: RBB vs Baringa

£ MILLIONS · FY2021 → FY2025 · £/PARTNER OVERLAID

View on a laptop for the interactive chart.

In this project file, both are partner-owned London LLPs with visible FY2021-to-FY2025 financial rows, and both grew fast over that window. That is where the similarity ends.

RBB Economics runs a concentrated partnership. The membership actually contracted, from 20 in FY2021 to 18 in FY2025, while revenue climbed from £61m to £108m. Profit per member rose from £2.02m to £3.34m, a 65 per cent increase spread across fewer people. Fewer owners, more each.

Baringa Partners runs the mirror image. Its partnership expanded from 98 members to 178 as revenue rose from £202m to £450m, and the firm also distributes roughly £170m in salaries to its 1,800 non-partner staff. More owners, bigger pool, distributed wider.

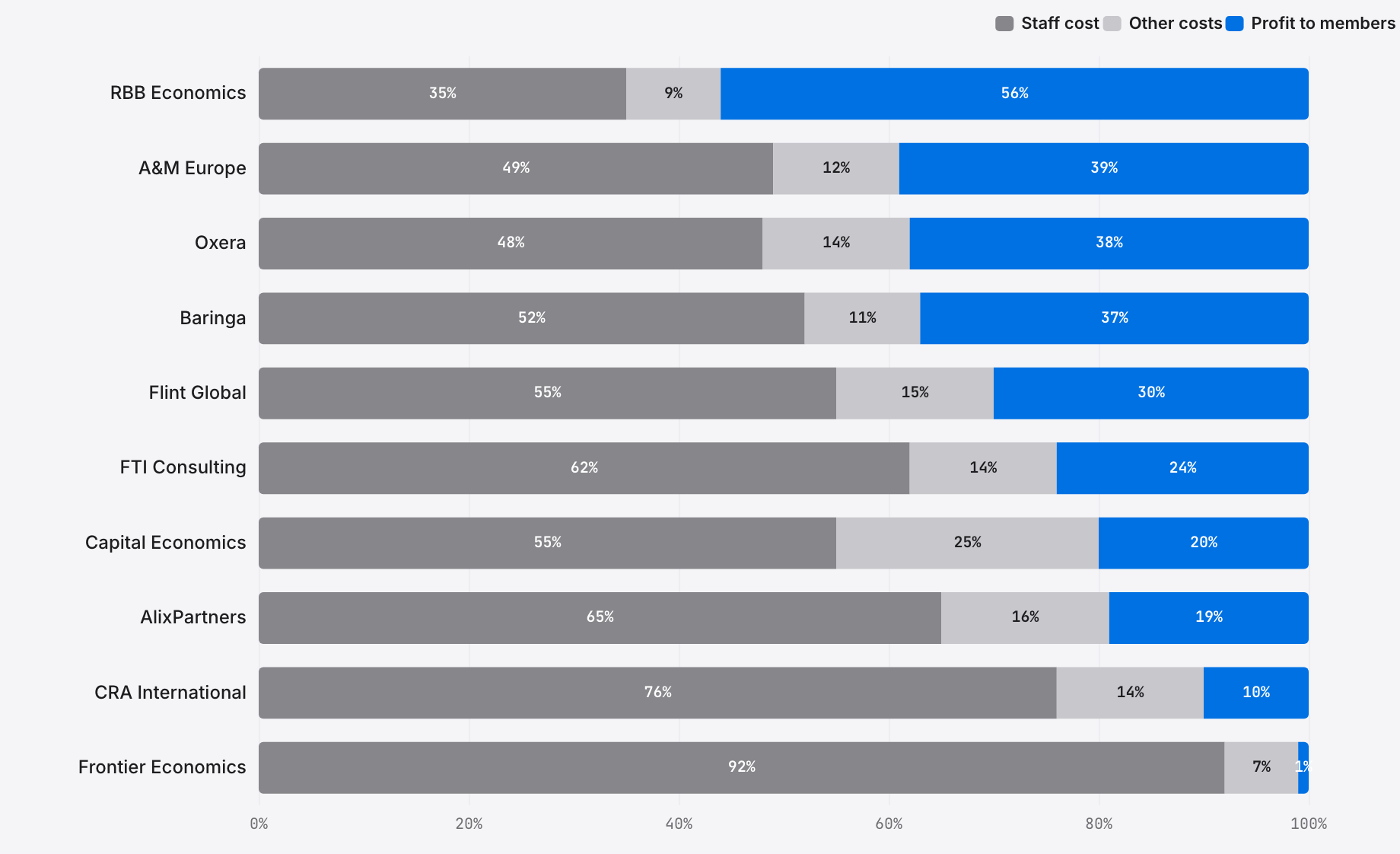

Revenue split: staff · other costs · profit to members

% OF REVENUE · TOP 10 FIRMS · FY24–25 · SOURCE: FILED ACCOUNTS

COST STRUCTURE

View on a laptop for the interactive chart.

The two growth stories above are one layer of the thing. The next filed-accounts chart uses the same project rows to split revenue into staff cost, other costs and profit to members.

RBB is the extreme. For each revenue pound, 56 pence becomes profit to its 18 LLP members; 35 pence pays staff; nine pence covers everything else, meaning rent, software, travel and professional indemnity. That is how a single partner ends up with £3.34m a year. A small, closed partnership taking a very large share of a medium-sized revenue base is the whole trick.

Frontier is the mirror image. 92 per cent of revenue is staff cost; one per cent shows up as profit to members. Frontier describes itself as employee-owned, and the accounts are consistent with a model in which partner economics flow through salaries and staff ownership rather than large residual distributions. The profit line, once again, is a residual by design.

THE DISPUTES MIDDLE

FTI Consulting, AlixPartners and A&M Europe land between 49 and 65 per cent staff cost and 19 to 39 per cent profit-to-members. They are large partnerships with deep pyramids under each partner, profitable by any normal standard but nowhere near the RBB extreme.

CRA International sits at the bottom of the table on a ten per cent operating margin. That is not inefficiency. CRA is a US subsidiary, and it remits most of its UK revenue upward to a Boston parent. A purely domestic LLP like RBB does not pay that cost.

CHAPTER 05

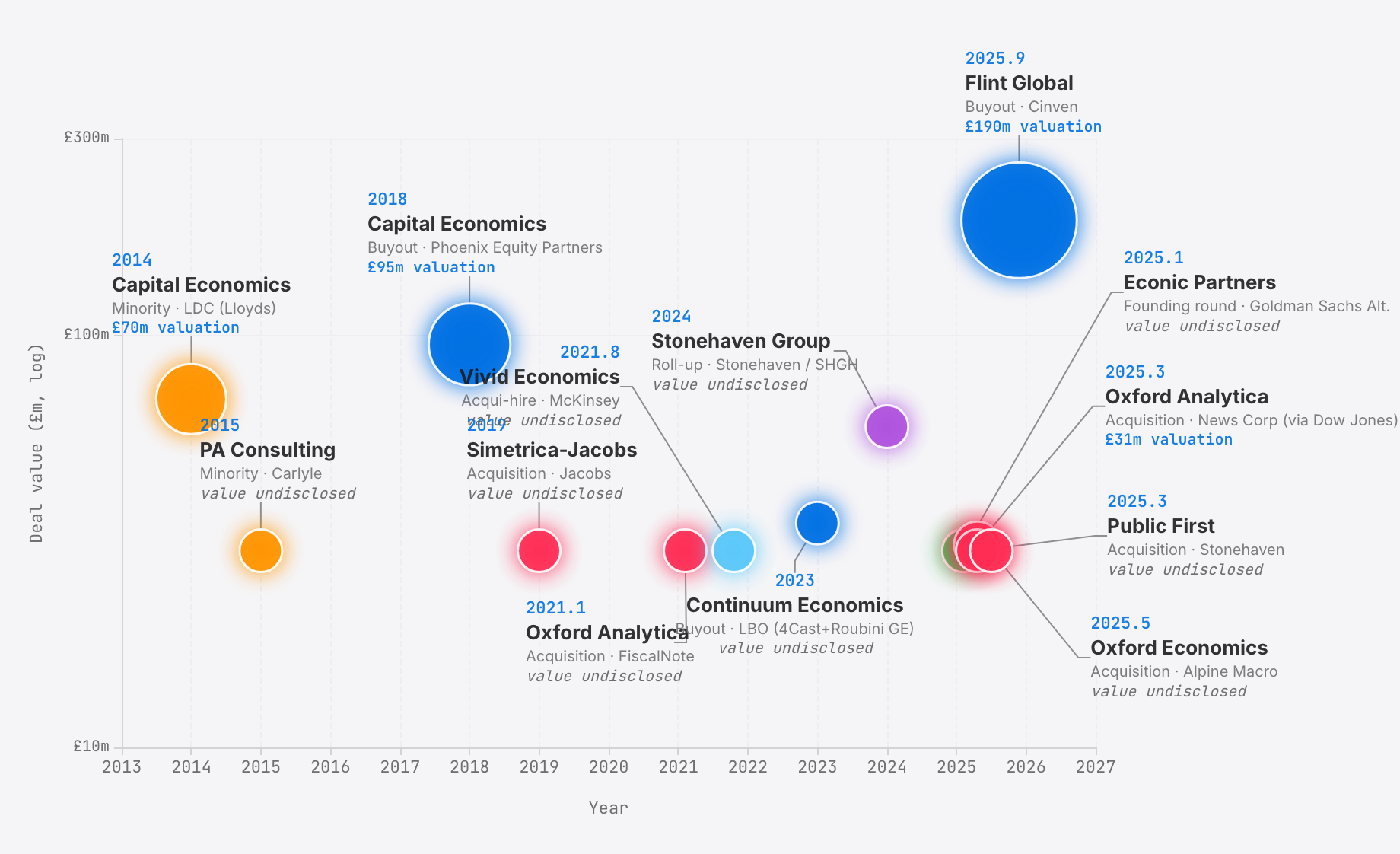

When the money arrived

The first private-equity marker in this project file is 2014. More followed.

In December 2025 Cinven agreed a majority investment in Flint Global; official terms were undisclosed; press reports put the deal at a ~£190m valuation (~16x EV/EBITDA), which the chart plots as a reported rather than filed figure. Ed Richards, the former Ofcom chief, and Sir Simon Fraser, the former permanent secretary at the Foreign Office, both remain on the cap table as shareholders. The project deal file also records Stonehaven's March 2025 acquisition of Public First, after an earlier 2024 Stonehaven roll-up marker. The cheques keep coming, but the exact public valuation evidence is thinner than the headline deal flow.

CHAPTER 06

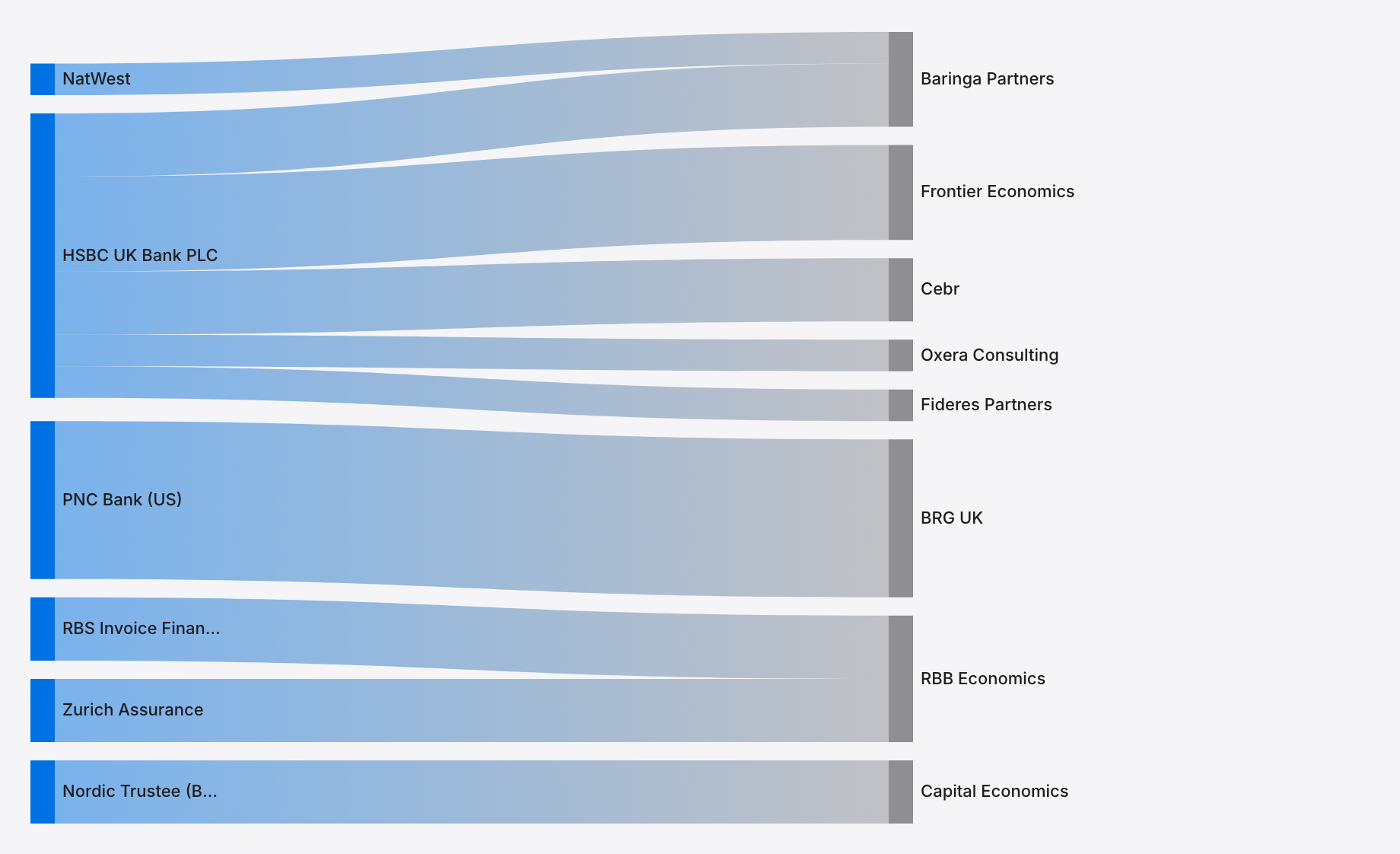

The debt map

50 outstanding charges across the industry. Here is who banks whom.

Outstanding Secured Charges

LENDERS → FIRMS · COMPANIES HOUSE CHARGES REGISTER

SANKEY DIAGRAM

View on a laptop for the interactive chart.

HSBC UK Bank PLC banks the UK economics industry. It holds charges against Baringa Partners, Frontier Economics, Oxera Consulting, Cebr and Fideres Partners, five visible names in the trade; the filings make HSBC a shared creditor across otherwise different economics and advisory practices.

BRG UK uses PNC Bank, which is American. Its US parent arranged the UK facility through its US banking relationships, and the London subsidiary took what it was given.

RBB Economics splits its charges between RBS Invoice Finance and Zurich Assurance. The Zurich charge is pension-linked.

Capital Economics is the oddity. Its Companies House charges point to Nordic Trustee, which represents bondholders rather than banks. The original Phoenix Equity Partners debt structure, charges in favour of Glas Trust Corporation Limited, registered between April and June 2018, was satisfied in March 2026 and replaced by new charges in favour of Ocorian Trustee (UK) Limited, trading as Nordic Trustee, registered in November 2024 and January 2025. Refinancing, secondary sale, or some combination of the two, the PE ownership structure is evidently evolving.

CHAPTER 07

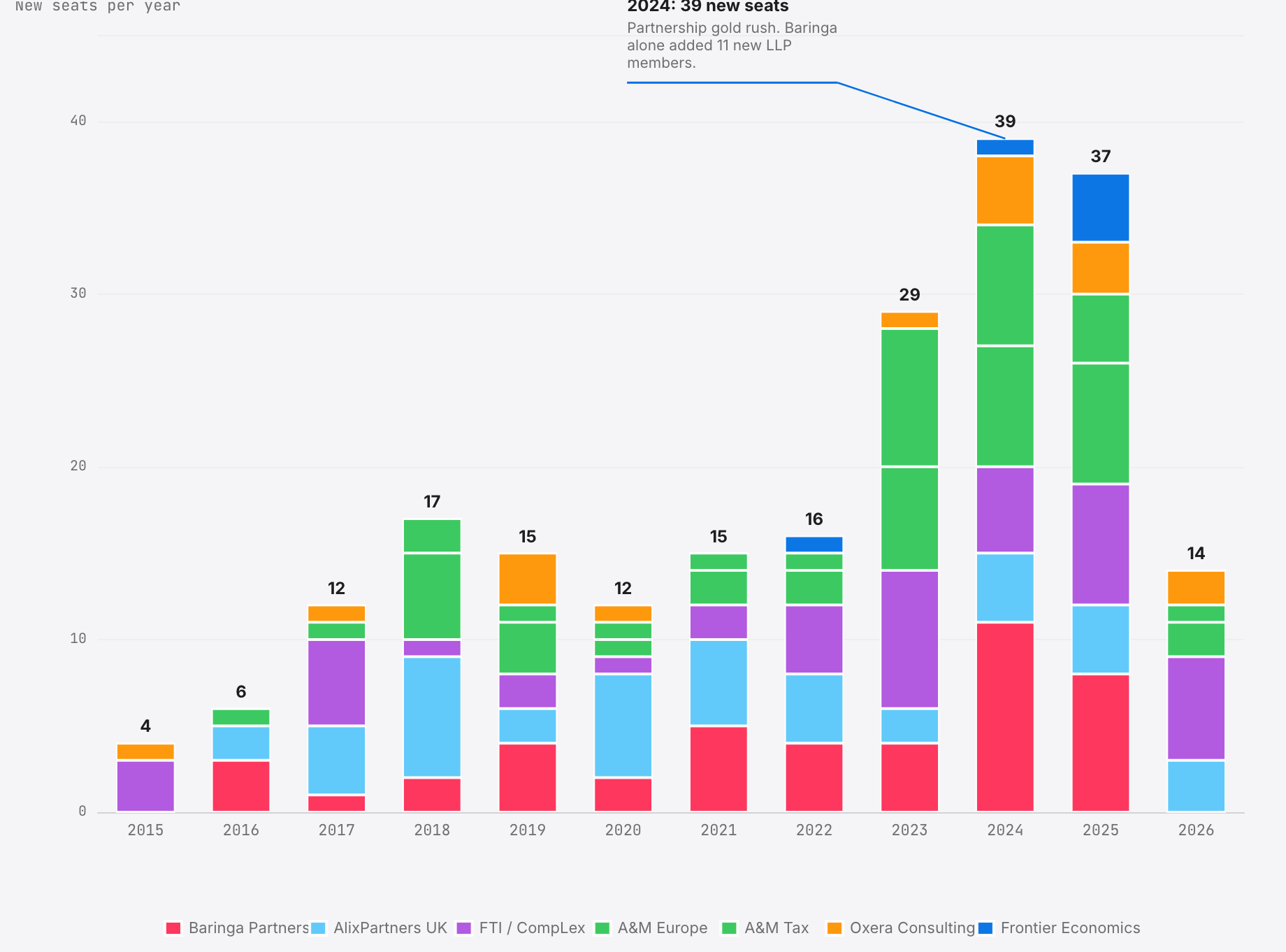

The partnership gold rush

New director and LLP-member appointments per year across seven selected large firms.

Director & LLP Member Appointments, 2015–2026

NEW SEATS PER YEAR · SOURCE: CH OFFICER APPOINTMENTS FILINGS

STACKED BAR

View on a laptop for the interactive chart.

The chart's break point is 2024. From 2015 through to 2022, the seven selected UK economics and disputes firms in this chart filed roughly 15 new director or LLP-member appointments a year. In 2024 that chart total jumped to 39; in 2025 it came in at 37. The plotted rate had more than doubled in 30 months.

Baringa led the chart, and A&M ran second. Baringa's bars show 11 new LLP members in 2024 and another eight in 2025, the largest single-firm contribution in this seven-firm appointment chart.

INFLOWS ARE NOT THE WHOLE STORY

The partnership is not merely growing, it is churning. In the same seven-firm chart, recorded departures also rise after 2022. The net chart draws the difference from the appointment-minus-departure constants below: in most years the seven firms gained somewhere between five and 15 partners on balance; in 2024, in this charted series, the net number crossed 20.

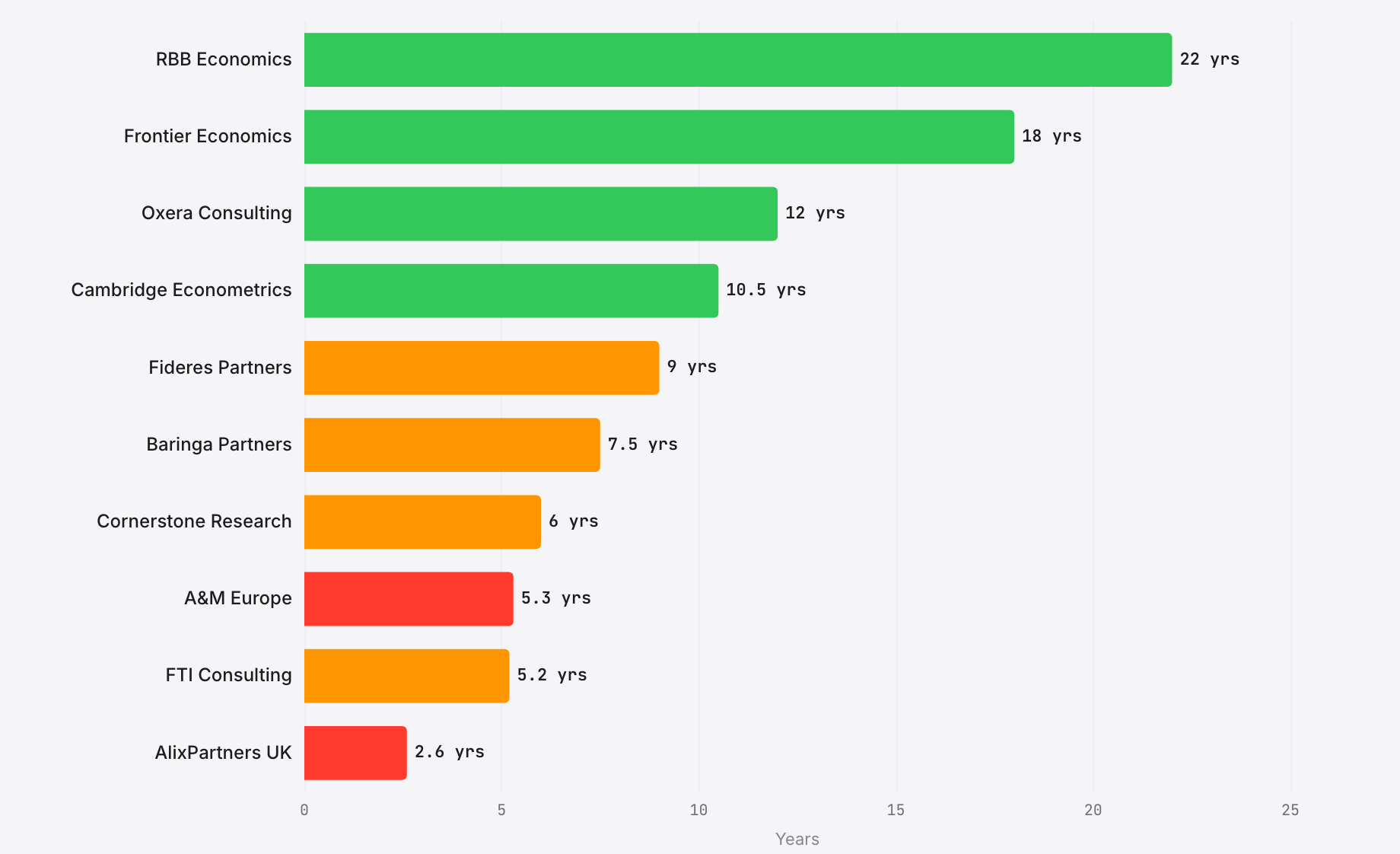

Average LLP-member tenure, by firm

YEARS · ACTIVE MEMBERS ONLY · SOURCE: 1,885 CH OFFICER APPOINTMENTS

WHO KEEPS THEIR PEOPLE

View on a laptop for the interactive chart.

The next panel turns from hiring to retention, measured here as the average tenure of LLP members still active at each firm today.

RBB and Frontier are the extremes in this chart. The active-member core at each firm averages 22 years on the partnership or directors' register at RBB and 18 at Frontier. The officer file records long continuity at both firms, while Vitaly Pruzhansky's resignation from RBB on 1 April 2025 is one visible partner-level departure in the recent window.

Oxera, Cambridge Econometrics and Fideres sit in the middle tier at 9 to 12 years in this tenure calculation.

THE CONVEYOR-BELT END

AlixPartners UK averages 2.6 years. A&M Europe is 5.3. FTI, taking in its Compass Lexecon subsidiary, is 5.2. In this dataset, those larger partner classes show shorter active-member tenure than RBB, Frontier, Oxera, Cambridge Econometrics and Fideres.

The gold-rush chart above tells you who is hiring. This one tells you who they are replacing.

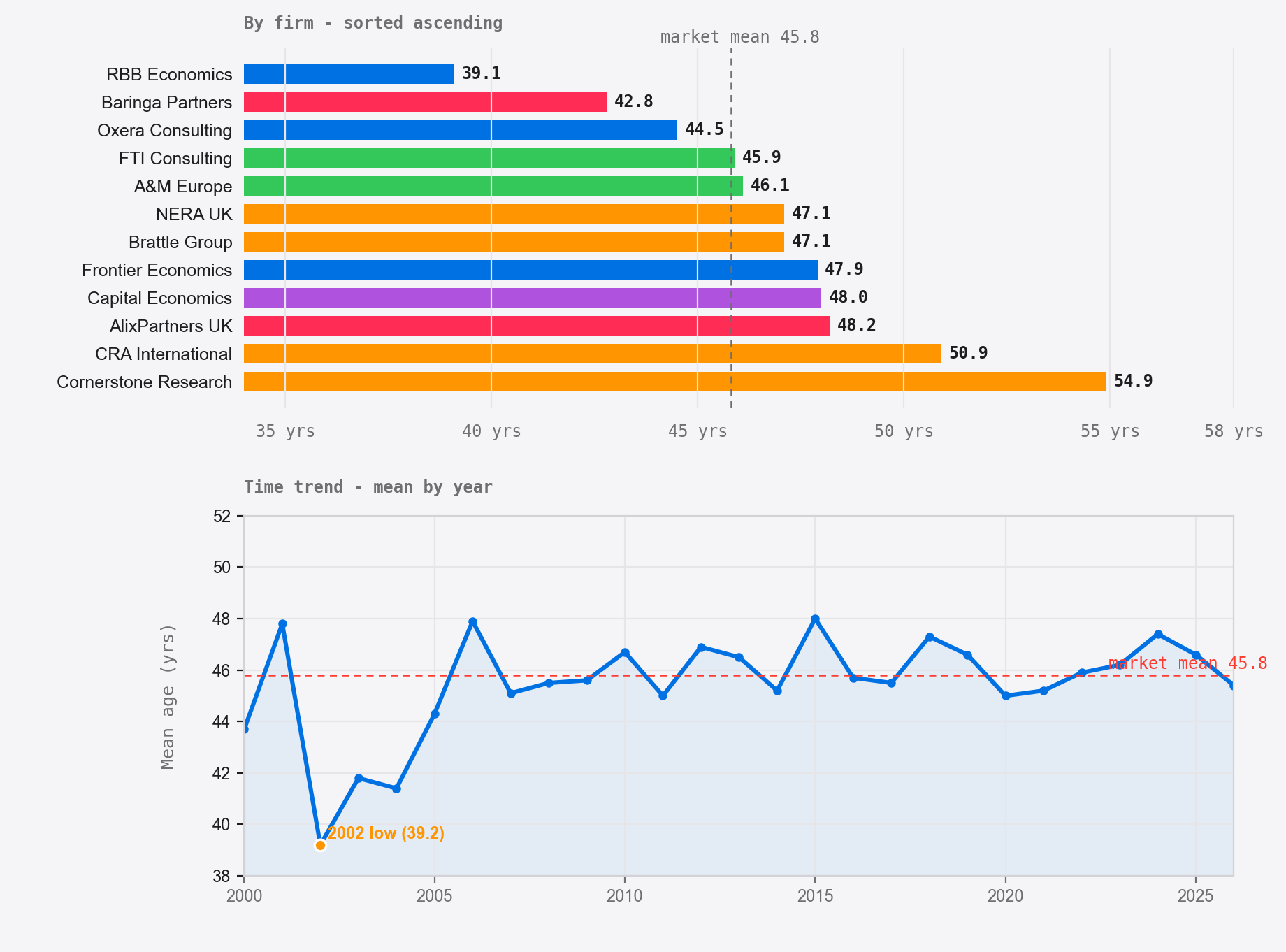

Age at appointment: when do they actually make partner?

MEAN AGE AT APPOINTMENT · 2000–2026 · 1,637 USABLE DATED OFFICER RECORDS

AGE AT APPOINTMENT

View on a laptop for the interactive chart.

Chapter 07 has asked who was hired and how long they stay. The final panel turns to age at appointment.

The time trend is almost flat in this officer dataset. Between 2000 and 2026 the mean age of a new director or LLP member in the UK economics consultancy market has hovered at 45 to 47 years. In the chart, the number barely stirs at the 2014 arrival of private equity or the 2024 appointment surge.

But firm-level variation is enormous. RBB Economics promotes people at an average age of 39. Cornerstone Research does not hire anyone under 46. That is a 16-year spread across firms that sell into the same regulatory proceedings, and it is structural, not coincidental.

The project data is not evidence of what clients reward, but it does show two appointment patterns. RBB grows its own: the mean age of 39 reflects partners who joined the founding cohort in 2002, plus a small number of later LLP-member appointments at roughly the same career stage. Cornerstone buys senior names off the shelf: the officer file shows later-age appointments, including former regulators, tenured academics and senior experts. The minimum age of 46 is a selection pattern in this dataset, not proof of a formal hiring rule.

Both routes produce expert-witness practices, but they produce different firms. The young-promotion model appears to concentrate institutional knowledge in a small, durable partnership; the senior-import model appears to maximise named credibility while producing shorter officer-tenure cycles. The middle of the chart, Baringa, FTI, A&M, Frontier, in the 43-to-48 range, looks more hybrid.

TWO PARADOXES

RBB is the youngest large firm in the chart and the longest-tenured. The reason visible in the project chronology is 2002: Ridyard, Bishop and Baker left NERA with 13 colleagues, a 16-economist founding cohort in all, and the subsequent officer file shows unusually long continuity.

AlixPartners is the oldest and the shortest-tenured in this chart. Its visible pattern is later-age lateral hiring and shorter officer tenure. Cornerstone Research takes the later-age pattern further: its minimum age at appointment in this dataset is 46.

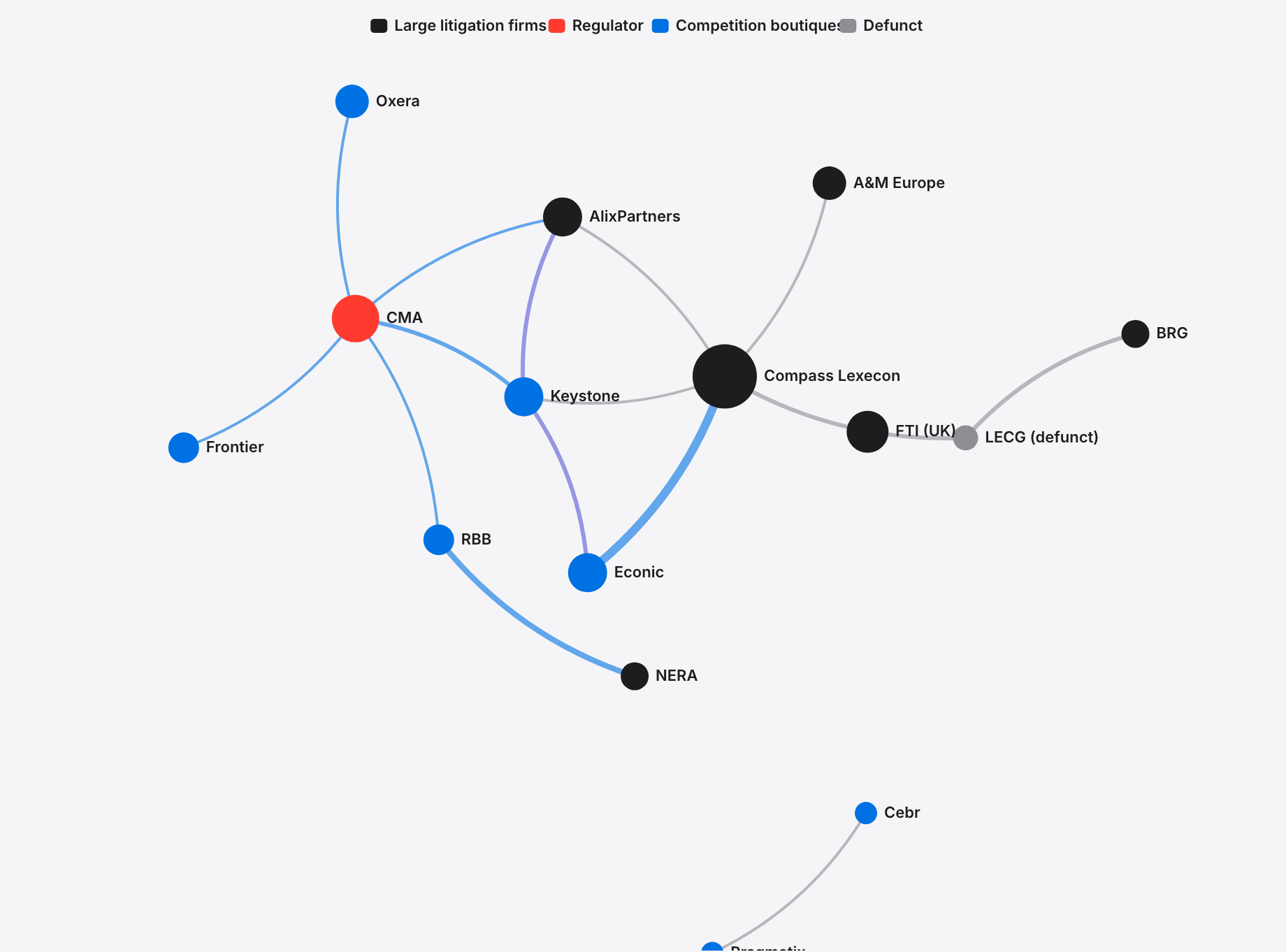

CHAPTER 08

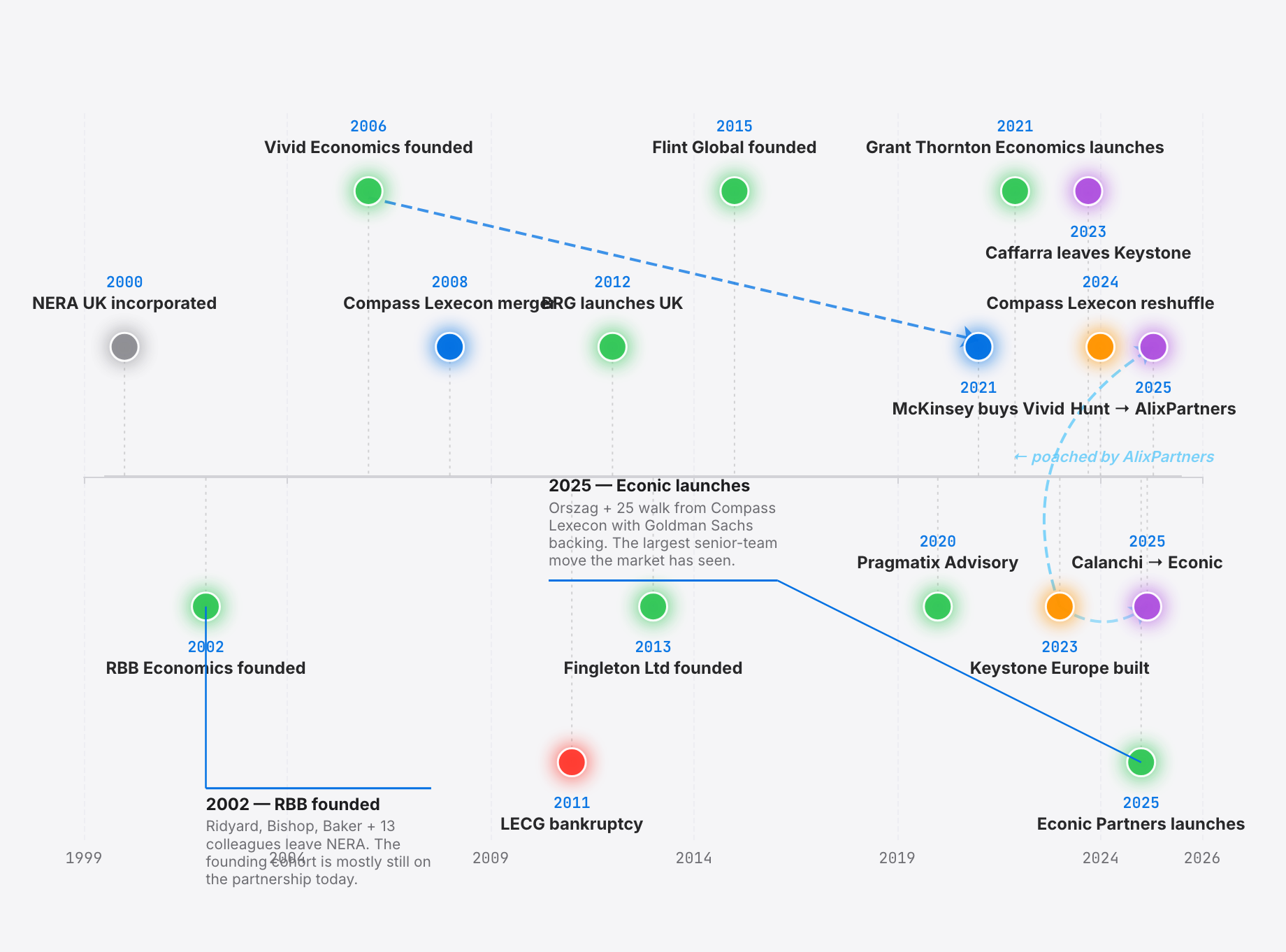

The founder tree

Selected events in the project chronology, 2000 to 2025.

EDGE WEIGHT = SHARED DIRECTORS / LLP MEMBERS 2000–2025 · FORCE LAYOUT

COMPASS LEXECON AS HUB

View on a laptop for the interactive chart.

The timeline above shows events. This chart shows the structure those events left behind. In this project network, an edge appears between two firms when the file records a shared director or LLP member since 2000.

Compass Lexecon is the hub of the documented UK economics-consultancy movement graph. Many firms are within one or two edges of it. The ribbon connecting Compass Lexecon to Econic Partners, the 25-plus economists named in Econic's February 2025 launch release, is the thickest edge in this dataset.

The CMA sits in its own satellite orbit. It has exit edges running everywhere, to Keystone, Oxera, Frontier, AlixPartners, and almost no return edges. The regulator is a net exporter of talent. It is not a marketplace.

THE ISOLATED TWO

Frontier and RBB are almost disconnected from the rest of the graph. Frontier has one documented edge in this senior-move file: Mike Walker's move from the CMA to Frontier, announced in October 2025 and effective 5 January 2026. RBB has one, Benoît Durand, a senior hire from the European Commission's competition side, who became an LLP member at RBB on 1 April 2011. In this dataset, both firms sit below two overlap edges. The tenure chart in chapter 07 is the other way of looking at the same picture.

CHAPTER 09

The competition-economics family tree

The microeconomics-and-regulation lineage, traced firm by firm from 1980, then the corporate ownership chain that ties FTI, LECG and the two Lexecons together. Both charts are reconciled to Companies House and to each firm's own published history.

UK economic consultancy: a family tree, 1980–2026

Press play, or drag the slider, to watch the industry grow. Vertical dotted lines mark major regulation; curved arrows show people moving from one firm to start or join another.

1980

UK-grown employee-ownedUS firm in LondonStrategic / regulatorySpecialist

Corporate ownership: how FTI, LECG and the Lexecons fit together

Several of the firms above are subsidiaries or successors of larger groups. Lexecon Inc (Chicago) and COMPASS were merged by FTI to form Compass Lexecon in 2008. LECG was the largest casualty: liquidated in 2011, with David Teece spinning out Berkeley Research Group the year before, and Jorge Padilla's European competition team joining Compass Lexecon as part of the dissolution.

Operating todayBrand absorbedLiquidated

Curved arrows on the first chart mark people moves between firms; on the second they mark corporate acquisitions and the LECG dissolution. Founding dates are reconciled to Companies House and to each firm's own history. Keystone Strategy is a US firm (founded 2003, Accenture-owned since 2020); the bar marks its London competition-economics build from 2022, not a UK founding.

8,293 filing events, 90 firms, one industry

The tracked UK economics consultancy dataset fits inside a single SQLite database that runs on a laptop. The laptop costs less than what an RBB partner earns in a morning.

90

Firms tracked

£2.48bn

Disclosed revenue floor

8,293

Filing events

1,664

Account filings

The firm-level financial and registry numbers in this story came from Companies House; market-size comparators and transaction notes are separately attributed where used. No firm was contacted; no interview was conducted; no informant was cultivated. The data was already filed, already indexed, and already public in the registry at Cardiff. The financial picture of a £2 billion industry turns out to be largely reconstructable from statutory documents alone.

The public catalogue is grouped into seven segments. Policy has 35 firms; regulation has 17; and macro forecasting has 16. Litigation and competition together account for 15 firms, including several high-revenue rows.

Block size is turnover, where turnover is visible. In this chart, the largest measured rectangles are the multi-practice advisory houses: FTI Consulting, Baringa and A&M. The pure-play economics shops, the boutiques that trade on formulas, expert reports and witness evidence, sit as medium blocks inside their own colour band.

The firms outside the disclosed-turnover set are carried as unsized rows where this project has no clean current turnover line. They appear in the treemap as identical uniform tiles, ranked by category rather than revenue.

The visible market is the measurable part. The rest of the catalogue still matters, but the accounts do not let it be sized cleanly.