The Profit Machine: 2020-2025, and the Next 25 Years

Part 5 of 7: an 18-partner competition-economics firm on a single floor of 199 Bishopsgate quietly booked the highest profit-per-partner visible in this project's Companies House sample of UK consulting LLPs with detailed accounts; McKinsey acquired Vivid Economics and Planetrics; Jacobs moved to full PA Consulting ownership at a £3.05 billion implied valuation; Econic launched with Goldman Sachs Alternatives funding. The filing trail sets the evidence base for the scenario discussion that follows.

The £5.77 million line item

RBB Economics LLP's FY25 accounts were lodged at Companies House on 23 January 2026, and note 8 recorded a member entitlement to profit of £5,771,775. The same accounts show £108.4 million of revenue, £61.0 million of operating profit, 18 members, and average profit per member of £3.34 million. The accounts do not name the member attached to the largest entitlement; the LLP disclosure gives the size of the entitlement, not the identity. In this article, it is treated as a disclosed line item rather than a named-pay claim.

Within the pure-play UK economics-boutique subset of this project's Companies House sample, no higher highest-paid-member line has yet appeared. Magic Circle law firms, global accountants, and the big strategy houses are outside this comparison because their statutory accounts do not usually disclose member-level remuneration in a form that permits a clean like-for-like read. A&M Europe LLP's latest accounts do show a larger cash figure, but A&M is a 73-member Europe-wide partnership sitting on €301 million of revenue. RBB's line is striking because it appears in a much smaller competition-economics LLP.

Part 5 follows the account rows from FY2021 through FY2025. Revenue rose from £60.7 million in FY2021 to £108.4 million in FY2025; members fell from 20 to 18; and profit per member climbed from £2.02 million to £3.34 million. 23 years after the 2002 walkout from NERA that Part 2 sets down in detail, the firm Ridyard, Bishop, and Baker built posted the highest profit-per-partner visible in this project's detailed-account LLP sample.

The base for the RBB and Baringa comparison is the FY2021-FY2025 account rows. The final section is a scenario read built from that base.

Section 1: Two firms, two arithmetics

Hold RBB and Baringa side by side over FY2021-FY2025. Both grew fast, but their member columns moved in opposite directions: RBB went from 20 members to 18, while Baringa went from 98 to 178. The difference matters because it changes what growth means for profit per member.

RBB Economics LLP, FY2021-FY2025

| Year | Revenue | Op Profit | Margin | Members | £/member |

|---|---|---|---|---|---|

| FY2021 | £60.7m | £40.8m | 67.2% | 20 | £2.02m |

| FY2022 | £62.9m | £39.6m | 62.9% | 19 | £2.06m |

| FY2023 | £75.0m | £46.2m | 61.7% | 19 | £2.40m |

| FY2024 | £82.0m | £44.0m | 53.7% | 18 | £2.41m |

| FY2025 | £108.4m | £61.0m | 56.3% | 18 | £3.34m |

Start at the Members column. RBB carried 20 partners into FY2021 and carries 18 now. Over the same window, revenue rose by 79 per cent. That is the arithmetic of the profit machine, and the margin profile tells the other half of the story. Through FY2024, operating margins drifted downward as the firm took on associates, opened new desks, and absorbed the cost of expansion; then in FY2025 the leverage appeared in the filed numbers. Revenue rose by £26 million year on year, operating profit rose by £17 million, and profit to members rose accordingly.

Two readings of that margin are consistent with the filings. RBB concentrates on competition work — merger control above all — where fees are least exposed to procurement pressure; and its filed revenue per head (roughly £378,000 in FY2025) runs some two-thirds higher than at the more regulation-diversified Oxera (£227,000), which is what high utilisation of a deliberately small staff looks like in accounts.

Baringa Partners LLP, FY2021 vs FY2025

| Year | Revenue | Members | £/member |

|---|---|---|---|

| FY2021 | £202m | 98 | £0.90m |

| FY2025 | £450m | 178 | £0.91m |

Baringa did the opposite thing. Revenue more than doubled; the partnership nearly doubled alongside it; and profit per member barely budged. The firm chose scale and distribution over concentration. Its FY2025 highest-paid-member figure is a derived estimate, not a disclosed absolute: note 12 says the highest-paid member was entitled to seven per cent of the £161.9 million discretionary profit pool, which gives roughly £11.3 million before any disposal-cash kicker. RBB grew revenue 79 per cent with fewer partners. Baringa grew revenue 123 per cent with 82 per cent more partners. Both are successful businesses; RBB is the more concentrated profit machine.

Section 2: The Vivid acqui-hire

In March 2021, McKinsey announced that it had acquired Vivid Economics. The press release called it an acquisition. The Companies House file calls it something different.

Vivid had always filed under the small company exemption: no revenue line, no segmental profit, no partner remuneration. McKinsey said the combined Vivid and Planetrics team numbered roughly 130 people across London and Washington, and the marquee names were visible in the source trail. Cameron Hepburn, the Oxford climate economist and co-founder; Robert Ritz, the Cambridge energy and competition economist who had built Vivid's carbon-markets and energy-transition practice. McKinsey wanted the team, and it wanted Planetrics, the climate scenario software Vivid had built. The subsequent Companies House record shows the UK legal entity being wound down separately.

What followed looks like acqui-hire mechanics. McKinsey took the Vivid and Planetrics bench into McKinsey Sustainability. Hepburn became a senior adviser while keeping his Oxford chair; Ritz joined as a principal; the Planetrics codebase transferred and the clients migrated. Vivid Economics Limited, a company that had existed since 2006, was left to go through the statutory liquidation process.

In August 2023 the shell entered Members Voluntary Liquidation. PwC took the appointment, Steven Sherry and Jen Whatcott signed the paperwork, and the company was dissolved on 27 May 2026, after the final meeting return. The public register preserves the liquidation history and a final set of small-company accounts that did not disclose what the firm had actually been worth.

The case is worth attending to because the statutory record is narrower than the market story. The filings do not show whether Vivid was a failed experiment or a successful team sale. They show a McKinsey acquisition announcement, a team and IP absorbed into McKinsey Sustainability, and a UK corporate wrapper later placed into solvent liquidation.

Vivid is one observed case, not a rule. It suggests one possible route: a Big 3 strategy house can buy an existing climate-economics team, absorb the people and IP, and leave the old corporate wrapper to wind down separately. Cambridge Econometrics (with its E3ME model), eftec, Aurora Energy Research, E3G: each has specialist climate-economics capabilities that could fit that route, though whether any of them are acquisition targets is speculation rather than evidence.

Section 3: The Jacobs thesis

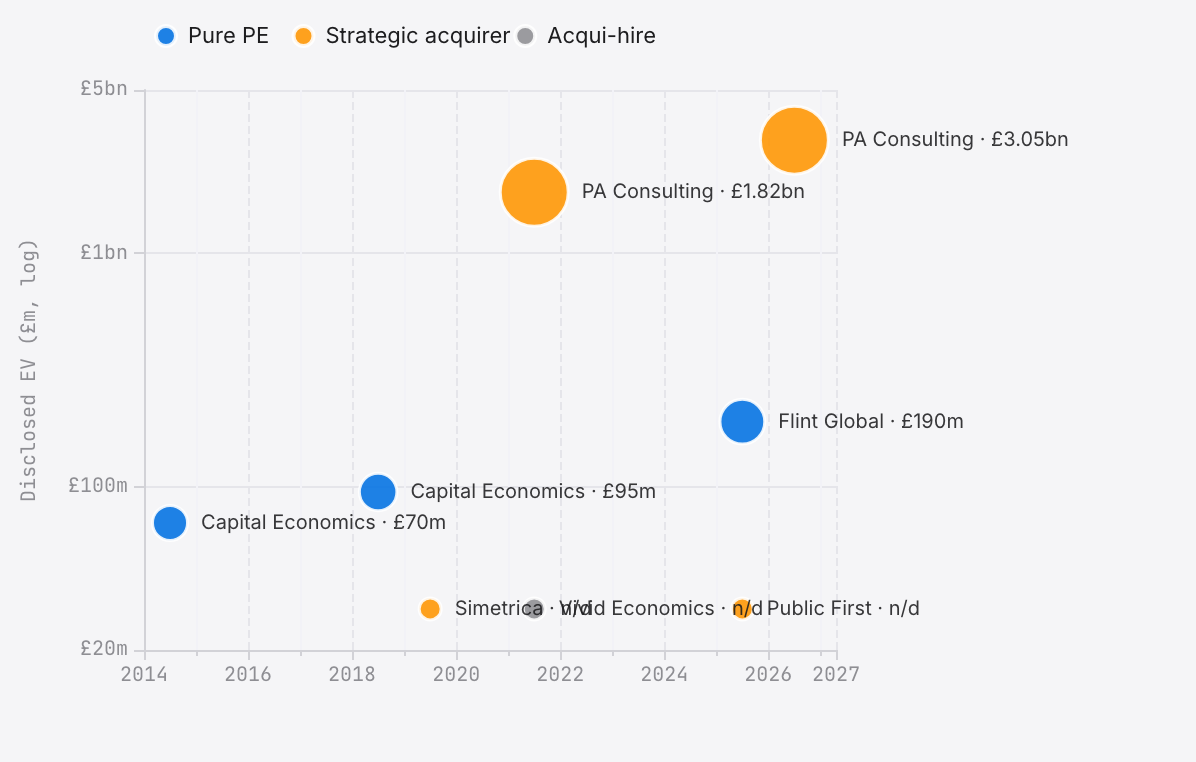

Dallas sets the price. In the seven years between 2019 and 2026, a New York-listed engineering company called Jacobs Solutions, twelve billion dollars of annual revenue (its Pentagon programme-management arm was spun off to Amentum in 2024), infrastructure advisory for Whitehall, assembled a large UK advisory position. The project deal file records three relevant transactions across the period: Simetrica-Jacobs, a 65 per cent PA Consulting stake, and then the remaining PA stake.

The first transaction was Simetrica. In October 2019, Jacobs took a 50-per-cent stake in Simetrica, a Hammersmith boutique founded five years earlier by Daniel Fujiwara to specialise in wellbeing valuation, the discipline of attaching a monetary number to social outcomes for Treasury business cases. The price was not disclosed. The firm was renamed Simetrica-Jacobs and kept trading from the Shepherds Building.

The second transaction was large. On 30 November 2020 Jacobs announced a 65 per cent majority interest in PA Consulting Group Limited, a four-thousand-person advisory firm headquartered at 10 Bressenden Place, behind Victoria Station; Jacobs later said the investment placed PA at an enterprise value of £1.825 billion. Carlyle, which had held 51 per cent of PA since the 29 September 2015 deal at a purchase valuation of roughly a billion dollars, exited. The remaining 35 per cent was left with PA employee rollover at closing, with Jacobs also describing a sweet-equity incentive pool for PA partners and employees. Overnight, PA Consulting, defence, digital, healthcare, UK regulated utilities, public sector, became the strategic core of Jacobs's European consulting footprint.

The initial Jacobs transaction still left the remaining 35 per cent with employees and former partners. The 2026 remaining-stake deal was the disclosed exit route for that holder group.

The third transaction was announced on 5 January 2026 and completed on 23 March 2026. Upfront consideration for the shares Jacobs did not already own: about £1.216 billion, paid 80 per cent in cash and 20 per cent in Jacobs stock. Deferred consideration: £75 million, payable on the second anniversary in shares, cash or a mix at Jacobs' election. Implied valuation for 100 per cent of the business: £3.05 billion. Implied multiple: 13 times expected calendar-2025 adjusted EBITDA before synergies, 12.3 times including estimated synergies. After completion, PA's ownership story sits inside Jacobs's New York-listed disclosure regime; UK statutory accounts remain part of the picture, but no longer the whole story.

The arithmetic carries a story that is easy to miss. On the two Jacobs valuation markers, enterprise value moved from £1.825 billion in 2021 to £3.05 billion in 2026, a 67 per cent uplift over five years, roughly eleven per cent annualised. Applying those whole-company valuations mechanically to the 35 per cent holder group implies an increase from about £639 million to about £1.07 billion before any adjustment for debt, expenses, dilution, tax or individual allocation. This is an arithmetic comparison, not a claim that every employee received the uplift; it is the proportional read of Jacobs's own disclosed value markers. The useful conclusion is narrower: the remaining-stake holders exited against a materially higher whole-company value than the 2021 entry marker.

data/pe_deals.csv.

This is not private equity in the conventional sense. Jacobs is a public company operating a long-horizon roll-up: no exit clock, no limited partners to repay, no two-and-twenty to service. In this reading, what it shares with the financial-sponsor cases discussed above is the thesis, that UK regulated-industry advisory work carries defensible margins and an ageing ownership base, and what differs is the vehicle. Jacobs does not return capital to investors. It absorbs companies into a global services business and keeps them.

This is the strategic-acquirer route. In the cases documented here, the pure PE houses buy, leverage, grow, and sell on a fund timetable. The strategic acquirers, Jacobs for the whole-firm route, McKinsey for the acqui-hire route, buy, integrate, and hold. McKinsey acquired Vivid Economics and Planetrics and then launched McKinsey Sustainability with the Vivid bench inside the platform; Jacobs bought a majority PA interest first, then the remaining stake, and kept running PA under the acquired brand. Same broad direction, different mechanics.

Three numbers finish the picture. Jacobs now owns 100 per cent of PA Consulting and 100 per cent of Simetrica-Jacobs. Jacobs presented the remaining-stake deal as margin-accretive and strategically tied to higher-value advisory and digital work; the £3.05 billion valuation is the cleanest disclosed benchmark for later UK advisory comparisons.

Section 4: Econic Partners, the story of 2025

In February 2025, Econic's launch release said Jonathan Orszag, Mark Israel, Kirsten Edwards-Warren and Catherine Barron had launched the firm with more than 25 economists. The release also said Goldman Sachs Alternatives and the Willig and Ordover families provided financing.

FTI's own investor materials put official numbers around the disruption. In the February 2025 earnings-call transcript, management said senior departures in the US competition part of Compass Lexecon could create substantial revenue and profitability headwinds and used $35 million as an order-of-magnitude reference point. In the Q1 2025 results release, Economic Consulting revenue was $179.9 million, down 12.1 per cent year on year, and the segment note records a 6.6 per cent decline in billable headcount.

The interpretation used here is deliberately narrower than the press drama around the dispute: expert-witness economics appears more person-attached than many other advisory businesses. That reading is consistent with FTI's official discussion of senior departures, with Econic's expert-led launch release, and with the project people ledger. It is not treated as a proven law of the market.

The family-investor detail matters. Robert Willig and Janusz Ordover co-founded COMPASS Lexecon's predecessor, COMPASS, in 2003; Compass Lexecon's own history says COMPASS and Lexecon combined in 2008. Econic's launch release then names the Willig and Ordover families among the new firm's investors. The founders' families are therefore on the opposite side of the 2025 breakaway from the brand their predecessors helped build.

The parallel to 2002 is useful but not exact. That year, as Part 2 narrates in full, Ridyard, Bishop, and Baker left NERA and built a partnership model in its place. By FY2025, RBB's filed accounts show a higher profit-per-member line than any NERA row in this project's UK filings.

Run the comparison through 2025 and the similarities are visible: a senior team leaves an incumbent; a new economics partnership is formed; clients and staff become the contest. The differences are just as important. Econic launched with institutional funding from Goldman Sachs Alternatives, while RBB began as a smaller NERA spinout. Any claim that Econic will repeat RBB's economics is a forecast, not a filing fact.

The 23-year gap between the two breakaways is a framing device, not a prediction. It makes the generational comparison worth asking, but the ledger cannot tell us whether the 2025 spinout ages like the 2002 one.

Econic's UK expansion has been, in the firm's own words to the legal press, aggressive. Hires from Compass Lexecon's Madrid, Brussels, and Berlin offices have followed the London anchor, and competing mandates on the same merger cases have already surfaced. The live question is whether the funded-breakaway model can hold the senior team and the case pipeline together.

Section 5: The firm-by-firm picture

The firms in this dataset run on materially different models, and their filed accounts reflect that. The snapshots below use the latest rows currently in the project ledger.

Different margins, different models

Brattle Group UK. Revenue of £39 million in FY2024, an operating loss of £0.9 million, and four outstanding charges on the Companies House register. Brattle's US parent covers the shortfall and the firm continues to hire, but the most recent UK filing shows the operation running at a small loss — £39.4 million of turnover against an operating loss of £0.9 million in FY2024.

Frontier Economics. Revenue of £97 million in FY25 (up from £86 million in FY24), with operating profit at £1.4 million in both years. Frontier is employee-owned, and the thin margin appears consistent with a model in which profit is distributed through salary and bonus rather than the residual operating line, though that reading is an interpretation of the accounts rather than a confirmed statement from the firm's leadership. The accounts do not show the kind of operating-margin expansion that RBB's do, but the ownership structures are not comparable: RBB distributes profit to 18 LLP members, while Frontier distributes value through staff share ownership.

High performers

RBB Economics. The outlier. Already covered. £3.34 million per member, the highest profit-per-member row in this project's detailed-account LLP sample.

A&M Europe LLP. €301 million of revenue, a €14.2 million top earner, and the largest disclosed member-entitlement figure currently captured in the database. A&M's Europe partnership is a much broader litigation, restructuring and advisory platform than the pure-play competition boutiques, so the cash number is not a clean like-for-like comparison with RBB.

Baringa Partners. £450 million of revenue, a top earner of roughly £11.3 million (a derived figure, seven per cent of the £161.9 million discretionary profit pool disclosed in note 12 of the filed accounts, rather than a disclosed absolute), 178 partners. In the project file, it is the clearest scale story: revenue rose sharply, but partner count rose with it.

Flint Global. £31 million of revenue, a 30 per cent operating margin. In 2025, Cinven agreed a majority investment; the official release did not disclose terms, but press reporting (Bloomberg) put the enterprise value at about £190 million, a reported ~16x EV/EBITDA — a reported, not officially confirmed, multiple.

Fideres Partners. A litigation economics specialist, growing fast off class action damages work in competition and financial services. Private, opaque, and increasingly visible in UK collective proceedings before the Competition Appeal Tribunal.

Interesting

Public First was acquired by Stonehaven on 25 March 2025, as part of Peter Lyburn's rolling acquisition of UK public affairs and policy advisory firms. Public First's founders Rachel Wolf and James Frayne stay on; the Stonehaven group now owns a substantial political and policy consulting stack in Westminster.

Oxford Economics had already begun its succession before John Walker, the founder, passed away in March 2026. In a leadership transition announced on 4 December 2025, Innes McFee took over as Chief Executive, Neil Walker was appointed Deputy CEO and joined the Board, and long-serving chief executive Adrian Cooper moved to Executive Chairman. The firm remains private, family-controlled, and a major independent macroeconomic forecaster in the UK.

Section 6: The shape of the whole

The curated universe contains 90 UK economics consultancies. The public directory gives 81 of them a direct Companies House number; the working database also carries registered, parent and brand rows for analytical continuity, including Compass Lexecon as a brand pointer to FTI Consulting LLP. Across the latest disclosed-turnover rows in that database, 30 firms sum to £2.48 billion (€/£ 0.85, $/£ 0.78). In the project ledger, that total is treated as an observed floor: many remaining firms file small-company, subsidiary, charity, academic or parent-consolidated accounts without publishing a clean practice-revenue line. As a sense-check, Cebr’s March 2018 estimate of £1.53bn for 2016/17, extrapolated forward at the 11.3 per cent CAGR they assumed, would imply roughly £3.6bn by 2025. The two numbers therefore bracket a £2.5bn–£3.6bn working range: a DB-observed floor and a Cebr-extrapolated upper bound.

On the structural fields the database actually holds, the 87 internal firm rows split as follows: 15 standalone LLPs, 8 Ltds with a disclosed parent, 63 other Ltds, and one brand pointer row (Compass Lexecon, pointing to FTI Consulting LLP).

Partner-owned LLPs

- RBB, Oxera, Baringa, FTI, AlixPartners

- A&M Europe, A&M Tax, A&M Disputes

- Fideres, Independent Economics, Macro Advisory Partners

- Plum, Reckon, Volterra, York Aviation

Ltd with disclosed parent

- CRA, Aviation Economics, CEPA, Continuum (4cast)

- ECA, London Economics (Indecon), Simetrica-Jacobs, WPI Strategy

Other Ltd (independent or unflagged)

- Oxford Economics, Capital Economics, Cambridge Econometrics, Europe Economics, DotEcon, Aether, Cebr, Public First, and other independent or unflagged companies in the directory.

Dual-seat directors

- Hold active director seats at two registered entities simultaneously — in every case sister companies within the same group (Capital Economics and its research arm; ECA Economics and Economic Consulting Associates). Genuinely cross-firm dual directorships do not appear in the register.

Status events, 2023–2026

- Vivid: entered MVL 2023; dissolved 27 May 2026.

- Econic: incorporated December 2024 (launched February 2025)

An earlier version of this page used a 24/12/39 split (Foreign-PE / LLP / Independent) sourced from public-domain ownership knowledge that the database itself does not yet capture; the true count of foreign- and PE-owned UK economics consultancies is plainly higher than the six the DB flags, but cannot be reconciled from the DB alone.

The long tail is the part nobody sees. In the current working database, 43 of the 87 CH-registered firm rows have no usable turnover figure in any extracted year. In the wider 90-firm public coverage map, 35 firms have financial rows but no usable turnover line, while 12 have no extracted financial rows yet or no clean standalone CH practice entity. Many are small teams serving regulatory or policy niches. Some may grow; many may remain too small or too opaque ever to publish a clean turnover figure.

The damages dividend

One demand-side shift maps closely onto the post-2020 revenue curves in this series: the rise of cartel-damages litigation. The European Commission's trucks cartel decision of 19 July 2016 imposed what was then the largest cartel fine in EU history, €2.93bn, on MAN, Volvo/Renault, Daimler, Iveco and DAF for fourteen years of price collusion, with a further €880m on Scania in September 2017. The fines were only the opening act: the follow-on damages claims ran through the UK Competition Appeal Tribunal for years afterwards, and the Supreme Court's Merricks v Mastercard judgment of December 2020 lowered the certification bar for opt-out collective actions, after which more than fifty collective actions were filed with the CAT. For economics consultancies this was a new production line. When the first trucks claim reached full trial, Royal Mail and BT v DAF (February 2023), the parties filed some 48 expert reports and spent twelve of the twenty-five trial days on expert evidence — Economic Insight's James Harvey for the claimants, a Compass Lexecon team under Damien Neven for DAF — before the Tribunal applied a “broad axe” 5 per cent overcharge and awarded roughly £39m. The Tribunal also remarked that both sides' expert conclusions were “clearly influenced in favour of the commercial interests of their respective clients” — a £39m verdict that doubled as a review of the industry itself. No firm discloses how much of its revenue comes from damages work, so the causal link to the filed growth in this series is an inference; but the timing, the expert-report counts and the firms' own marketing of dispute practices all point the same way.

Section 7: Six forces, 2025-2050

The next section is a forecast, not a filing fact. Six forces are already visible in the evidence above.

Six forces, 2025-2050

- Generational succession. The series spans firms founded or reshaped across RBB (2002), Frontier (1999), Oxera (1982), Capital Economics (1999) and Oxford Economics (1981); Oxford Economics had already announced a named leadership transition before John Walker's death in March 2026. The visible examples already split into routes: Oxford Economics passed leadership to Innes McFee and Neil Walker; Flint agreed a PE majority investment; Vivid sold to a strategy house. More founder-led firms may face versions of those choices.

- Econic against Compass Lexecon. The live question is whether Econic becomes an elite breakaway at scale or whether Compass Lexecon defends its incumbent position. The pattern from the NERA-RBB split points one way; Compass Lexecon's long record and corporate backing point the other. This is a watch item, not a settled conclusion.

- What AI does to the practice. Competition economics, litigation damages, and market modelling may be exposed in different ways. Expert witness work, where a partner's personal reputation signs the report, looks relatively insulated. Computational modelling, where models like Cambridge Econometrics's E3ME and the CGE frameworks used elsewhere do the heavy lifting, may thrive as AI extends what one modeller can do, or come under pressure as general-purpose AI tools replicate more of the core work at low marginal cost. Policy evaluation sits in the middle.

- Climate economics consolidation. McKinsey's Vivid acquisition gives one clear precedent. Cambridge Econometrics has model IP; eftec has regulatory credibility; Aurora Energy Research has data and energy-market reach. Those traits make the green-consulting space a plausible consolidation field, but which buyer moves next is a scenario, not a filing fact.

- Buyer pluralism. Section 3 laid out the two categories already active: financial sponsors that buy, grow, and sell, and strategic acquirers that buy, integrate, and hold. Mid-sized founder-led specialists such as Cebr, Europe Economics, Aether and DotEcon fit the kind of profile buyers may study, but any target list is an analytical watchlist rather than evidence of a sale process. (Update, March 2026: Capital Economics' own PE debt structure has evolved. The original Phoenix-era charges to Glas Trust Corporation Limited were satisfied in March 2026, replaced by new charges to Ocorian Trustee (UK) Limited, trading as Nordic Trustee, created November 2024 and January 2025, consistent with either a refinancing or a secondary PE transaction. The template is not static.)

- The Big Four economics practices. Deloitte, PwC, KPMG, and EY run economics arms, but the project ledger does not identify separate statutory revenue rows or standalone public P&Ls for those practices. Whether these practices grow into proper economics brands or are absorbed into generic advisory is the open question. The evidence is not strong enough to say which remain distinct brands.

Closing

This is the industry visible in the project ledger between 2000 and 2025. It started with NERA as a central incumbent and Frontier Economics barely a year old. It ends with RBB Economics posting the highest profit-per-partner visible in this project's detailed-account LLP sample; with a Goldman-backed spinout already ranked Elite in its first year of existence; and with a disclosed-revenue floor above £2 billion for a market that remains obscure outside the sector.

A future edition of this series would probably start from the same raw material: Companies House filings, LLP disclosures, PSC ownership records, and transaction announcements. The story is likely to be different. The public evidence trail should still be audited accounts filed at Cardiff, year after year, by firms that most people have never heard of, sometimes producing partner economics that rival far better-known professions.

The ownership-market point is easy to miss from the outside. Some economists spend decades at NERA, Oxera, Frontier, Compass Lexecon or RBB, rise to senior management, and decide whether to stay inside the institution or build the next one. The cycle started in this series with Ridyard, Bishop, and Baker. It continues now with Orszag and Barron at Econic. A later edition may have different names.

Part 6: The CMA Drain

Part 6 follows the CMA-to-consultancy moves, Keystone's European leadership churn, AlixPartners' competition-economics hiring, and the wider revolving door through Ofgem, Ofcom, DG Competition, and the Treasury.

Read Part 6 →